Road TO Recovery Playbook | Weekly Market Commentary | March 16, 2020

After recording two double-digit drops in equity prices over the last three trading days, the global pandemic of COVID-19 has sent world equity markets into bear market territory. The result is a cumulative 30% drop in the S&P 500 Index in just under 30 days. Though daunting, once the market finds a bottom, which is where the index begins to consistently move higher than the previous market low—and we believe it is “when” not “if” the market finds a bottom—it may provide an attractive opportunity for long-term investors to consider adding risk to portfolios.

Given all the uncertainty, which can raise questions and result in emotional reactions from many investors, LPL Research believes that it is important to take a systematic approach to determine when that bottom might be found, enabling markets to reverse course and move higher. To guide long-term investors toward what to focus on in order to hone in on that timing and those potential buying opportunities, LPL Research has compiled a Road to Recovery Playbook.

LATEST PERSPECTIVE

These are extraordinary times. The global pandemic has caused significant worldwide economic disruption, driving stocks into a bear market for the first time in over a decade and sending U.S. Treasury yields plummeting. Major US cities have effectively gone into quarantine, entertainment and sporting events have been cancelled, large gatherings of people have been banned, schools have closed and the list goes on.

While the health of those close to us remains our top priority, as investors, we also must try to assess the economic and market impacts. Recession odds have risen sharply, as it is becoming clear the impact on economic growth and corporate profits—though temporary—may be significant. Powerful monetary and fiscal stimulus actions and more aggressive containment measures may likely help mitigate the impact, but it’s tough to see the other side from where we sit today.

THE PLAYBOOK

Before getting to our investor playbook, we would first encourage long-term investors to consider staying with your long-term investment plans.

We believe having a systematic playbook to follow can help us manage through these tough times. When those difficult times are caused by bear markets, a playbook can make clear what to watch as “leading indicators” of a potential market bottom that may signal the start of a sustained move higher. This playbook may help ease concerns by taking some of the emotion out of investment decisions and facilitating a measured approach. We all want to know when and where the market will bottom, the likelihood of a potential recession, and when the outbreak will be contained. These are extremely difficult questions to answer—but this playbook is designed to provide some clarity.

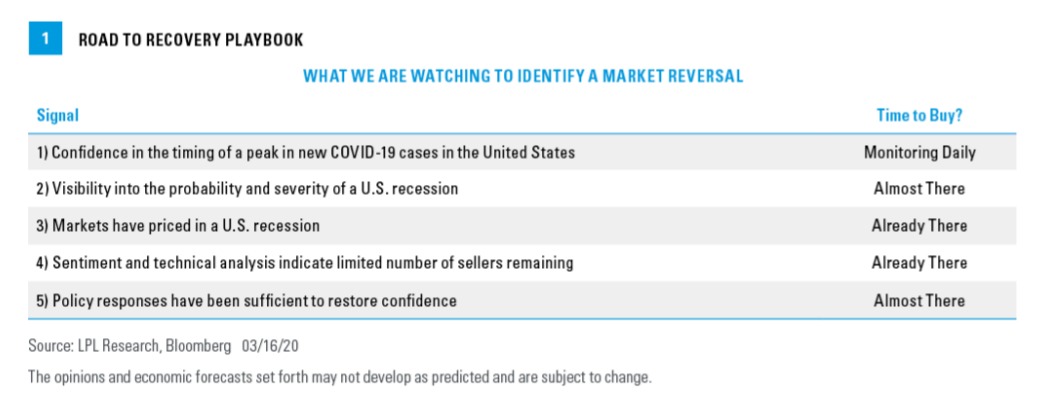

Foremost, we need to identify the most important signals, shown in Figure 1, that can help us determine when the market may find its footing. It’s important to note that having all five of these signals turning positive is not required before attractive entry points might be considered. Currently, the majority of these signals are either already or close to signaling that a potential bottoming process may not be that far off.

KEY SIGNALS FOR THE PLAYBOOK

Confidence in the timing of a peak in new COVID-19 cases in the United States. The number of new US cases continues to rise, and we don’t know when or at what level they will peak. Based on the experiences in China and South Korea, we think the peak is coming within the next month. However, the experience in Italy suggests perhaps it could take longer. The key is not to wait until the peak in new cases has materialized, but rather developing the confidence in the predictability of the pandemic’s outbreak path using sophisticated epidemic models, like Farr’s Law, which has successfully modeled disease spread through populations in past pandemic episodes. We see confidence in the timing of a peak as a major milestone in the stock market bottoming process as in past pandemics, the market has usually found its trough in prices tied to the stabilization of new cases, not necessarily the visibility of declines. We continue to monitor new cases daily and watch for signs of what path the US may take to.

Visibility into the probability and severity of a US recession. We won’t know for sure if the US economy has entered a technical recession for many more months—since you only know you’re in a recession in hindsight. However, we will likely see data that indicates the timing and severity of a potential recession very soon. We will be watching the most timely data points to help gauge the depth and severity of a possible recession, including the March Institute for Supply Management (ISM) surveys, consumer confidence, jobless claims, and the Leading Economic Index, among others.

Has a recession already been priced into markets? We think we are already there on this one. A nearly 30% decline in the S&P 500 Index from the February 19 record high is consistent with a typical recession. We can also point to valuations. For example, if we cut current S&P 500 earnings by 10% and apply a reduced price-to-earnings ratio (P/E) of 15, we get to an S&P 500 level of about 2,200, which we think is a reasonable recession-level downside target. We can also look at the equity risk premium, which is the difference between the earnings yield (earnings-to-price ratio of E/P rather than P/E) and the 10-year US Treasury yield. At over 5%, the equity risk premium is nearing the 6% level seen at the market lows in 2008–2009.

Sentiment and technical analysis indicate limited number of sellers remaining. To assess whether most aggressive sellers have been forced out of the market, we can look at investor surveys or technical indicators. Survey data such as the CNN Fear & Greed survey and the American Association of Individual Investors (AAII) survey reflect some of the most negative readings ever registered, a potential contrarian signal that most of the selling pressure could be behind us. Additionally, a historically high number of stocks are oversold, potentially a bullish combination when combined with the extreme negative sentiment.

Will policymakers’ response be sufficient to restore confidence? We think we are getting close to getting this signal. The Federal Reserve is pretty much “all in,” having effectively cut interest rates to zero while adding another round of quantitative easing (buying bonds) and more liquidity to ensure credit markets function. We have a very aggressive monetary policy, but what is needed now is a strong fiscal policy response, including targeted support for individuals and businesses most impacted by the crisis. We expect meaningful progress to be made this week in Washington, D.C., toward what could eventually exceed $500 billion in total stimulus.

Overall, we are getting closer to reaching all of these conditions, and an inflection point for the direction of markets may be approaching. You can hear us discuss more details of our Road to Recovery Playbook in the March 16 LPL Market Signals podcast.

REVISED ECONOMIC FORECASTS

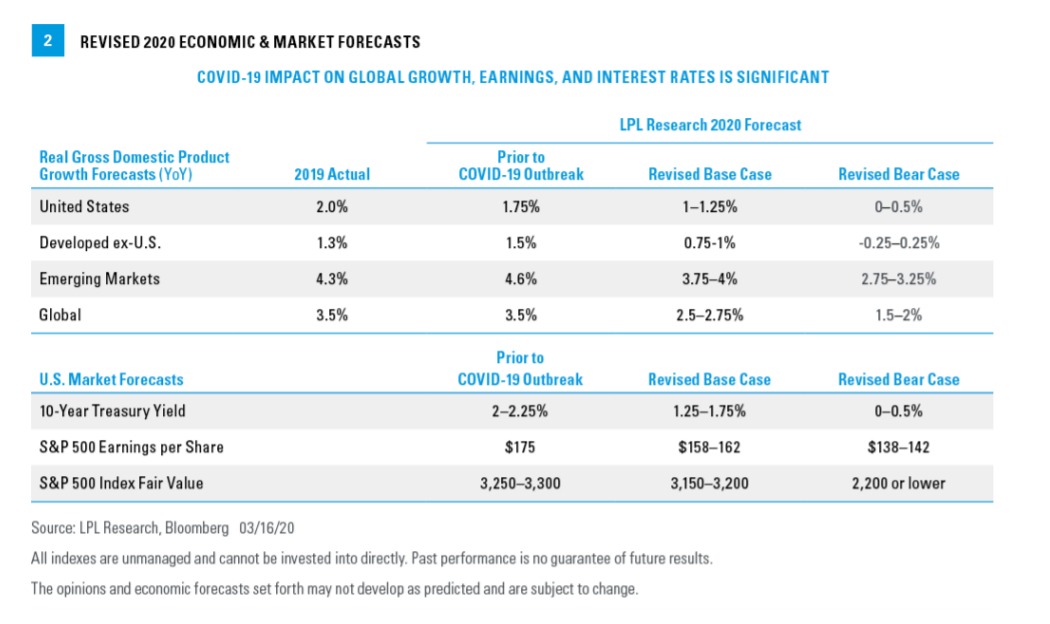

In response to the impact of the pandemic on the economy and markets, we have updated our forecasts for 2020 [Figure 2]. We have lowered our gross domestic product (GDP) forecasts for the US, emerging, and developed international markets, as well as global GDP. These forecasts reflect a greater than 50% chance of a short-lived economic contraction in the United States. We believe the strength of the US economy prior to the outbreak may help it weather the storm.

We have also lowered our forecast for the 10-year Treasury yield, S&P 500 earnings per share (EPS), and year-end S&P 500 fair value.

We have provided our base case as well as a potential bear case, given the amount of uncertainty. Our base case GDP forecasts are all slightly below consensus expectations, based on Bloomberg forecasts where available.

Our revised S&P 500 EPS forecast of about $160 is well below FactSet’s slow-to-adjust consensus estimate of $173.

Finally, our revised year-end 2020 fair value target for the S&P 500 of 3,150–3,200 is based on a P/E of 18, supported by lower interest rates and S&P 500 EPS in 2021 of $175, a slightly above-average earnings growth forecast for next year coming off potentially depressed profits in 2020. Investors may have to wait longer for those earnings in 2021 to come through, and the outlook is clearly uncertain, but we have more confidence in next year’s earnings than this year’s. In a recession scenario in which earnings may be heavily impacted, we may see a downside scenario on the S&P 500 of around 2,200 or potentially lower.

We will continue to review and expand on our thought processes behind these forecasts in next week’s Weekly Market Commentary.

CONCLUSION

We believe stocks have fallen to levels that are very close to a market bottom such that the next phase would be an upward-trending market. At that point, we would consider the environment very attractive based on our assessment of economic and market fundamentals. At that point, we would be thinking about upgrading our equities recommendation to overweight from market weight, which we lowered from overweight in March 2019 after stocks got off to a strong start to the year. But we want to err on the side of caution, which is where our playbook comes in. We will continue to monitor new COVID-19 cases, economic data, and policy news to determine an appropriate time to make an adjustment.

For now, our best advice for long-term investors would be to consider staying the course while we wait for more signs of progress in terms of the market’s bottoming process. We will continue to keep you updated on our views on the economy and markets on the LPL Research blog and other LPL Research communications as this difficult situation develops. From all of us on the LPL Research team, we wish all of you and your families the best of health. Everyone please stay safe.

Click here to download a PDF of this report.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The P/E ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher P/E ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower P/E ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

Please read the full Outlook 2020: Bringing Markets Into Focus publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

If your financial professional is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

Tracking # 1-966737 (Exp. 03/21)

Recent Posts

Navigating Strategic and Tactical Investment Horizons: The Differences | Weekly Market Commentary | March 10, 2025

Earnings Season Recap: Strong Growth, Big Upside, Now What? | Weekly Market Commentary | March 3, 2025

Refinancing ZIRP | Weekly Market Commentary | February 24, 2025

Tariffs Ignite a Metals Melt-Up | Weekly Market Commentary | February 18, 2025

Key Pillars of the Bull and Bear Cases in 2025 | Weekly Market Commentary | February 10, 2025

U.S. Exceptionalism: Is It Still Intact? | Weekly Market Commentary | February 3, 2025

Is the Bond Market Worried About Inflation? | Weekly Market Commentary | January 27, 2025

Categories